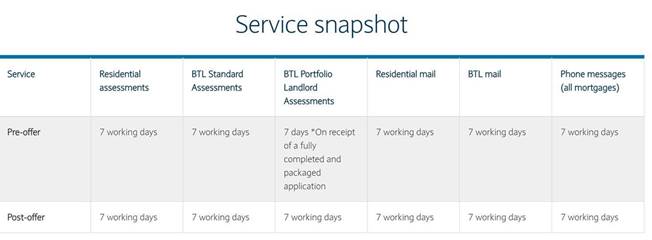

1 – Our Current Business Service Levels – Life has been really busy over the past few weeks with really healthy levels of Applications being received (thankyou) – in order to try and keep these to a manageable level and to offer you and your client the best possible service Service Levels currently stand at 7 working days (see below).

Important Note(s)

- Packaging Guide – In order for your application to be assessed and worked as quickly and seamlessly as possible please try and fully package when submitting, this will ensure that your case has the best possible chance of going to offer when the underwriter reviews it. I have attached the most recent Packaging Guide which you may want to use to check against before submitting to speed things up? Perfect Packaging Guide

- Attestation Form – Was introduced a few weeks ago and supports any Identification / Address or Declarations need for the case and is a great tool to negate the needs for some documents to be signed – if your case requires ID and Address confirmation please always attach an Attestation form to support this – I have attached a copy for your records above.

- Booking Desk – In order to manage the flow of applications that can be worked upon we did implement a “Booking Desk”– when you look to submit your application the system will automatically let you know if we have reached capacity for the day or whether we can take the application – if we have reached capacity please save your application and re submit the next morning.

2 – Loan-to-Income (LTI) multiples – So that we continue to lend responsibly during this unprecedented period of uncertainty, we’ve made some changes to our loan to income multiples that taken affect immediately and are already built into the Mortgage Calculators and Application system –

- The minimum income required for 4.49x multiple where LTV is greater than 90% has increased from £50,000 to £60,000;

- The minimum income required for 5.0x multiple where LTV is less than or equal to 85% has increased from £50,000 to £60,000;

- The minimum income required for 5.0x multiple where LTV is less than or equal to 80% has increased from £30,000 to £60,000;

- Minimum income required for 5.5x multiple for Springboard applications has increased from £50,000 to £60,000.

3 – Interest Only and Part & Part changes

Interest Only:

- We have removed the £200k minimum loan size

Part and Part:

- We have increased the maximum LTV from 75% to 80%

Note: for part and part, this does not change the existing maximum LTV limits for the Interest Only portion of the loan (50% max LTV and £300k minimum equity requirement for sale of property repayment strategy, and 75% max LTV for other repayment strategies, such as sale of stocks and shares).

4 – Time with current employer – It is no longer a requirement that non-Barclays customers be with their current employer for 3 consecutive months prior to application. Instead all applicants must have been employed for 3 months prior to application but not necessarily with the same employer. In call cases where the time with current employer is less than 3 months a full 18 months’ employment history will need to be recorded and the application will refer for manual assessment so the underwriter can review the customers track record. Consideration should be given to the applicant’s previous and current occupation and industry. Underwriters have discretion to request additional information/documentation.

5 – Housing benefit – When assessing affordability Housing benefit can be considered if the benefit will continue after the new mortgage completes. Note that in the majority of residential purchase applications the benefit will cease when the customer moves out of rented accommodation and, in those cases, should not be considered sustainable.

6 – All Things Springboard – Springboard has proved to be very popular over the past few weeks with more and more clients looking to use the higher loan to value option to get on the housing ladder – in order to fully understand how this works and how it may benefit your customer I have attached some of the relevant guides that should help you understand the concept further – in summary though here are some of the benefits –

· Available for first-time buyers and home movers for loans up to £500k (excludes new builds)

· Up to 5.5x income multiples for clients earning more than £60k

· Terms available from 5 to 35 years

· If all mortgage payments are made, helpers get their money back after five years

· Helpers still earn interest on their savings during the five-year period

For further information on how Springboard –

- Click here for the “Springboard” Website

- Click Here for your Full Springboard Guide

- Click Here for your Clients Springboard Guide

My support/ Escalations –

I have been supporting many of you whilst in isolation, I do have access to the back end of our systems and can check case progression, documents etc if you need any support and are having trouble getting through to the normal Broker Support Line – it would be good if you check with Broker support initially on 0345 073 3330 and then if you struggle to get through by all means drop me an e mail or phone call and I will do my best to help you. I do now have the ability to “Escalate” cases that have breached our published service levels or where we need to intervene – so please do let me know if you need any help here also. Finally I am also still running some proactive calls with many of you ensuring you are up to date with our current operating model, policy, products etc… please let me know if you would like a 20 min update call and I will book one in for you at a convenient time.

I just wanted to say a big thanks for your patience and working with us in these hard times. If you have any questions, need any help or support please do give me a call or drop me an e mail on 07825377098 / dewan.khan@barclays.com I will do my best to help you through the next few weeks and as always very much value your business

Keep well and have a good week ahead