When communicating with clients, please be mindful that including personal data in standard emails (such as names, addresses, DOBs, mortgage details, or account numbers) carries security risks. Unencrypted email can be intercepted, misdelivered, or accessed if an account is compromised, potentially leading to a GDPR breach.

When communicating with clients, please be mindful that including personal data in standard emails (such as names, addresses, DOBs, mortgage details, or account numbers) carries security risks. Unencrypted email can be intercepted, misdelivered, or accessed if an account is compromised, potentially leading to a GDPR breach.

It is fine to send general market updates, confirm appointments and also use their name, providing there are no other personal identifiers.

Wherever possible, encourage clients to use the OMS client portal. Your clients can safely send secure documents to you this way and can read any updates you make visible in a secure way.

If email must be used, you should ensure files are encrypted before sending.

Having completed our due diligence process we are happy to recommend Mailock from Beyond Encryption as the preferred solution.

Why This Matters

As a regulated firm, you’re required to ensure that any communication containing personal, sensitive, or financial data is protected. Secure email is a practical step toward fulfilling your obligations.

We have assessed Mailock against key compliance, usability, and integration criteria. The platform:

- Encrypts emails and attachments, protecting client data in transit.

- Allows you to verify recipients’ identities before granting access.

- Provides a full audit trail, helping to demonstrate your compliance efforts.

- Can be used with Outlook and your web browser, making it easy to adopt.

- Enables clients to respond securely without creating an account.

Mailock is already in use across many firms in the industry, and it has been recognised for its focus on regulatory compliance and client experience.

How to Get Started

We have secured a Connect Mortgages Member price of £8.50 per user/month, making it both a compliant and cost-effective choice.

This rate has been negotiated on your behalf, but each firm will contract directly with Beyond Encryption the providers of Mailock.

To take advantage of this offer or learn more, please click below:

Connect Mortgages Mailock Trial Registration

Alternatively, join a live Webinar and see Mailock in action:

Join a 30-minute webinar hosted by Carole Howard from Beyond Encryption on 2nd September at 11:00 am to see how Mailock works in practice and ask your questions live:

Register for the Mailock Webinar 02.09.25

For any further information: Carol Howard, Beyond Encryption Carole.Howard@beyondencryption.com

+44 20 8123 4546 | 07929750654

Regards

Alan Baldwin

Director of Compliance & Operations

For any questions or queries, contact the Compliance Team

Call : 01708 676110

he Financial Conduct Authority (FCA) expects principal firms to exercise effective oversight and supervision of their appointed representatives (ARs) to ensure compliance with regulatory requirements and prevent harm to consumers and markets. Key expectations include:

- Pre-Appointment Due Diligence – Principals must conduct thorough checks before appointing an AR, assessing its financial stability, business model, and the competence of its senior management.

- Ongoing Monitoring – Principals must regularly review their ARs’ activities, ensuring they remain compliant with FCA rules. This includes risk assessments, audits, and scrutiny of financial promotions.

- Clear Responsibilities & Controls – Principals must set out clear policies, training, and procedures for ARs, ensuring that they act within their scope of permissions.

- Data & Reporting – Principals must collect and analyse relevant data on their ARs’ performance and compliance, reporting key issues to the FCA when necessary.

- Intervention & Termination – Where issues arise, principals should take swift action to address concerns, which may include terminating the AR arrangement if necessary.

Effective controls and continuous adviser monitoring are at the core of our Network’s regulatory requirements. A dedicated Compliance department is essential to ensure the quality and performance of our Authorised Representatives (ARs).

While regular file reviews, grading, annual observations, and Fit & Proper assessments might be challenging, they are crucial for demonstrating ongoing competence and achieving the best customer outcomes.

In addition to these measures, the FCA mandates that Networks promptly address any breaches and report them. Although this aspect of the process is not always welcome, strict adherence to FCA guidelines is non-negotiable.

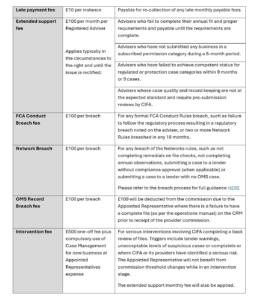

To ensure clarity about the rules and the consequences of non-compliance, below is a list of the fees that may be applied. The most effective way to avoid these fees is to consistently follow the guidelines.

These fees are as follows:

If you have any questions about any of the above, please do not hesitate to contact the Compliance team, who will be happy to help: compliance@connectmortgages.co.uk

Regards

Alan Baldwin

Director of Compliance & Operations

For any questions or queries, contact the Compliance Team

Call : 01708 676110

Email : compliance@connectmortgages.co.uk

Following feedback from advisers, we’re pleased to confirm that you can now send Terms of Business letters through DocuSign using OMS.

This new process brings several key advantages:

- Faster turnaround: Documents can be sent and signed quickly, reducing delays.

- Up-to-date documentation: The system ensures that the latest version of the Terms of Business is always used.

- Clear audit trail: There is a complete record of when the document was sent, received, and signed for compliance and accountability.

To be able to use this automated TOB, you will have first needed to have updated your fees in the loan details tab in OMS and put the case to the correct stage, full information on this is covered in the below training video.

To help you learn this new process, Member Support have prepared a training video that takes you through all the steps required to send your client a TOB via OMS. Click on Image below view.

Should you have any further questions, please do not hesitate to contact Member Support who will be happy to help. membersupport@connectmortgages.co.uk

Regards

Alan Baldwin

Director of Compliance & Operations

For any questions or queries, contact the Compliance Team

Call : 01708 676110

Email : compliance@connectmortgages.co.uk

With lenders being more and more risk adverse when it comes to evidence of income, it is important to ensure you are reviewing the documents and can identify potential issues and seek clarification before you proceed.

So, what are the most common areas we see on a payslip that could cause a lender concern?

- Net Pay. Does the net pay match what is being paid on the bank statement? This will almost never be different and if it is, you should ask for an explanation and evidence if available.

- Payment Method. Is the method of payment the same on the payslip as the bank statement? Payslips will confirm how they will be paid, i.e. BACs, CASH or Faster Payment and this should then match the bank statements. If this doesn’t the lender will almost certainly question this.

- Employee Number. Most payslips will have an employee number on them, this is usually given in order of when people joined the firm, so if someone has an employee number of 1, this will normally indicate they are the owner. A quick check can be to look at the employees start date and look at when the company was set up on Companies House. For example, if someone joins a company that has been in place for a number of years, their employee numbers will be quite high.

- Pension Contributions. Most people will have pension contributions included in their payslip, although, people can opt out of this. So, if you see this, ensure you are asking to a reason why.

- Consistency. Payslips will almost always look consistent between months, unless the company has changed software. Therefore, you should be looking out for differences between the payslips you have been given.

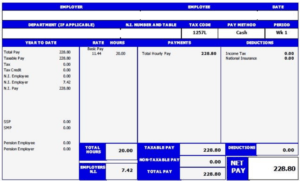

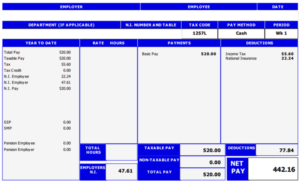

Look at the example below and see if you can spot anything that you would query?

Did you spot it?

Considering this is a payslip for the same company for the same week, they should match, but they don’t.

- In the Rate/ Hours section, one has the Basic Pay and number of hours, and the other is blank. Considering this is the same company, the two documents should be identical.

- In the payments section, one has the wording Total Hourly Pay and the other just has Basic Pay. If this wasn’t a joint application, this would be very difficult to spot, so you do have to pay close attention.

- The other issue with this, although you could not spot it, was the fact that the pay method for both was Cash, however, if you reviewed the bank statements, you could see they are paid via bank transfer.

These differences, without any explanation from the adviser, were enough for the lender to decline this case.

If you are ever unsure, you can always ask for copies of their tax documents from the Government Gateway which confirms the amount of tax and NI they pay per month, if this matches the payslips, this will help confirm the pay is genuine, but it isn’t a guarantee.

If you are ever unsure, you can always ask a member of the Compliance department who will be happy to help.

Regards

Alan Baldwin

Director of Compliance

For any questions or queries, contact the Compliance Team

Call : 01708 676110

Email : compliance@connectmortgages.co.uk

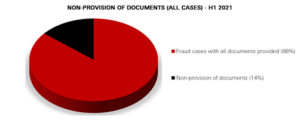

Compliance has checked 500 cases so far this year, so what are the trends that we can learn from?

Last year we enhanced our file checking process and introduced some new initiatives:

- Phone calls to deliver file check feedback

- Heads up process to help new (BLUE) advisers with their learning journey

- Improved file checking scoring system

- Compliance 1-1’s

So far, our new approach has been well received and we have seen an increase in the amount of advisers achieving Competent Adviser Status (CAS). But as well as this we are seeing less repeat mistakes and a steady improvement in the overall file quality.

From the 500 cases, what scores do we typically see?

If you were not already aware, below is what the gradings mean:

- 6-Green Advice is suitable, and the file is complete with no missing documents or information.

- 5-Green Advice is suitable, but there are minor fact-find omissions or document omissions (not minimum standard documents) but the omissions are not affecting the advice.

- 4-Amber Advice is suitable, but some documents evidencing advice are missing, or the suitability letter is presented with minor omissions.

- 3-Amber Advice is suitable, but one or more company standard minimum documents are missing, or the suitability letter is presented to the customer with material omissions on the recommendation, requiring re-issue.

- 2-Red Unsuitable advice, eg. mortgage unaffordable, product does not suit customer needs, justification for the advice is not clear.

- 1-Red Suspected fraudulent case, e.g.Back door residential, staged income, fraudulent documentation etc.

So, the typical score we see files graded as is Amber 3, which 50% of the cases checked have been graded, this means that the advice is good, but the cases require some amendments or there are some missing documents. However, it is also worth noting that 33% of cases are graded Green, which shows that generally case quality is very good.

If you are unaware of what the minimum standard documents are, there is a process in the Operations Manual in BOX HERE

What trends do we see from file checks that are making cases Amber?

Missing documents is the biggest reason for seeing Amber cases, the main documents being:

- Incomplete or missing proof of deposit, especially with gifted deposits

- Sanctions Searches not being completed

- Missing Credit Reports

- Insufficient Proof of Income, such as missing payslips

- Fees being charged that are higher than Connect’s fees tariff. If you are unsure of what Connect’s fees tariff, you can read it HERE

We also see a number of Terms of Business (TOB) that are old versions. We will from time to time update documents within the Operations Manual; therefore, it is important that you refer to these in each case. We have recently updated our Terms of Business, so please ensure you are using the latest version.

The easiest way to pass a case is to use the File Check tab on the case, this will cover all of the documents and other requirements you need to pass a case.

Should you have any questions on this, please do not hesitate to contact myself or the compliance team.

Regards

Alan Baldwin

Director of Compliance

For any questions or queries, contact the Compliance Team

Call : 01708 676110

Email : compliance@connectmortgages.co.uk

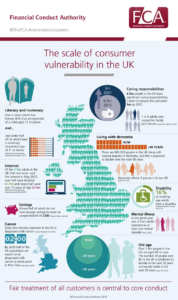

Most people have heard of the term vulnerable customers, and even know what type of people may be classed as vulnerable, but do you know what to do when someone is identified as vulnerable?

Before we cover what help can be given to vulnerable customers, let’s look at who might be vulnerable and the scale of how many people are actually classed as vulnerable.

The FCA definition of vulnerable

A vulnerable consumer is someone who, due to their personal circumstances, is especially susceptible to detriment, particularly when a firm is not acting with appropriate levels of care.

For the FCA’s full guidance on vulnerable customers, please read HERE

Vulnerability can come in many guises

Many people assume vulnerable people refers to the elderly or disabled, but in fact, vulnerability can come in many guises, such as:

Age (young and old): Someone who is young could be vulnerable due to having less experience in life making them more susceptible to fraud or manipulation. Someone who is old, or just older than the person they are talking to may struggle with terminology or technology.

Mental health: In any given year, one in four adults experience at least one mental disorder and may then find it difficult to deal with their finances. You may see erratic spending on their bank statements or missed payments on their credit report.

Physical health: 16% of working age adults have a disability. This may result in them finding it difficult to so simple tasks such as post a letter or answer the phone.

Low literacy: One in seven adults has literacy skills that are expected of a child aged 11 or below. Many people are having to talk to brokers in their second language and may struggle to understand important parts of the mortgage advice process.

Life changing events: Such as illnesses to themselves or a family member, or are going through a divorce or the even the death of a friend or family member. These events could result in unusual behaviour such as anger or crying over the phone.

Caring responsibilities: More and more people have caring responsibilities for family members, which means they may struggle financially or with just time to deal with other matters.

Financial hardship: Almost half of adults do not have enough savings to cover an unexpected bill of £300. Also, 1 in 2 adults in the UK with debt problems has mental health issues.

The Scale of Consumer Vulnerability in the UK

What to do

So, what should we do when we identify someone as vulnerable and what impact will this have on them being able to get a mortgage?

A useful tool to help follow the correct process is the TEXAS model.

TEXAS was originally developed following a study on mental health and debt collection, but it has become a tool that is used across the sectors to handle a wider range of vulnerable situations.

It helps ensure staff record:

- the most relevant information about characteristics of vulnerability,

- how these characteristics affect support needs, while

- helping to meet data protection requirements.

The steps of the model include:

- T Thanking the customer for their disclosure.

- E Explaining how their disclosed information will be used.

- X Depending on the basis on which the data will be processed either: eXplicit consent is sought or cheXs (‘checks’) are made to ascertain if the customer objects to data processing.

- A Asking the customer questions to find out key information to understand the situation better.

- S Signpost to internal support, or to external services with specialised expertise (where this is appropriate).

So, how does this look in practice?

When you identify a client who is vulnerable, firstly, you thank them for letting you know, because it is never easy to discuss these types of things.

Then you explain to them that now they have explained what vulnerabilities they have, what you will do with that information, such as note it on their file, so they won’t have to explain to anyone else. This includes the lender so they can continue to provide appropriate support. Following Consumer Duty, more and more lenders are asking for us to let them know if a client is vulnerable as they want to ensure they treat the customer fairly and appropriately. It is important to let the client know that the lender will not exclude the customer from any services due to their vulnerability.

Now the customer is aware of how this information will be used, you seek their permission to use it in this way.

So long as the customer is happy for you to register them as vulnerable, you should ask what help they will need? For example, if English isn’t their first language, do they need you to speak to a family member or send further details in a letter so then can take more time to review it.

Lastly, in some cases, they may need help beyond what you can offer, and in these situations the client should consider speaking to an expert. There are many free support charities or advice lines who can help with many situations, or they could discuss their issues with their doctor who can provide appropriate medical advice.

Just because someone is classed as vulnerable, does not mean they should be excluded from your services.

Being vulnerable doesn’t mean they should not get a mortgage, being vulnerable just means your client may need additional time or support from you to help them.

If you would like any further information on vulnerable customers, you can also read Connect’s Vulnerable Customers Policy HERE

Should you have any questions on this, please do not hesitate to contact myself or the compliance team.

Regards

Alan Baldwin

Director of Compliance

Call : 01708 676110

Email : compliance@connectmortgages.co.uk

The risk from AI (Artificial Intelligence) fraud has significantly increased recently with the advances that have been made in AI technology.

AI is being used to help in financial services with many lenders now using AI to help speed up the underwriting process, but as well as the benefits, there are also risks.

What is AI Counterfeit?

AI counterfeit refers to the use of artificial intelligence technologies to create fake or forged items, documents, digital content, or representations that are intended to deceive.

This practice leverages the advanced capabilities of AI to replicate, imitate, or generate items that are indistinguishable from the original or genuine articles. The concept of AI counterfeit encompasses several areas:

Deepfakes: Perhaps the most well-known form of AI counterfeiting, deepfakes involve using AI algorithms, especially deep learning, to create highly realistic and convincing fake videos and audio recordings. These deepfakes can mimic real people saying or doing things they never actually said or did.

Forgery of Documents: AI can be used to replicate or create counterfeit documents. With sophisticated analysis of style and technique, AI algorithms can generate forgeries that are challenging to distinguish from authentic items.

Digital Identity Theft and Fraud: AI can be used to mimic personal traits, such as handwriting, voice patterns, and facial characteristics, leading to identity theft and fraud in digital spaces.

Can you spot the real from the fake?

Below are two passports, can you spot which one is genuine?

In fact, both have been generated using AI.

Since Covid, businesses have implemented many non-face to face processes which are still in place today. Instead of customers showing you their documents which you can then make a copy of, they will instead send you scanned copies without you having to have met them in person.

So how can you verify they are genuine?

Check for inconsistencies: AI-generated documents may have inconsistencies in the layout, font, or alignment. Look for any irregularities in the text or images.

Inspect the photo quality: AI-generated photos might appear too perfect or lack natural variations seen in genuine ID photos. Look for signs of artificiality such as overly smooth skin, unrealistic lighting, or unnatural facial expressions.

Verify security features: Genuine passports and driving licenses often contain security features like holograms, watermarks, and special inks. Check for these features by tilting the document under light or examining it with a magnifying glass.

Examine the details: Look closely at the personal details such as the name, date of birth, and address. AI-generated documents may contain unrealistic or nonsensical information.

Compare with known samples: If possible, compare the document in question with genuine passports or driving licenses to identify any discrepancies in design or content.

Use technology: There are various online tools and software available that can help identify AI-generated images. You can use these tools to analyse the document for signs of artificial manipulation.

Seek professional assistance: If you have doubts about the authenticity of a document, seek assistance from experts such as law enforcement agencies or document verification services.

Some lenders will require you to have the documents verified by a professional such as the post office who provides this service, but just because the lender hasn’t asked for this, doesn’t mean you can’t ask for this yourself.

So, if you have any doubts, you can ask your customer for the original documents or for certified copies. No genuine customer will refuse to do this, when a customer does refuse to provide you with information, that is quite often a sign of fraud.

Where lenders are not asking for verified copies of documents, this may mean that they are verifying the customers’ ID electronically. This is a good way to help combat this type of fraud and why we use systems such as RedFlag which also verifies customers’ ID.

One last tip

If you are unsure if a document is genuine or not, ask Compliance. On many occasions we have had bank statements that looked like they may have been tampered with, which we reviewed ourselves and on cases where we were still unsure, asked the banks directly. They will then check the statements for us and let us know if anything has been amended.

Regards

Alan Baldwin

Director of Compliance

For any questions or queries, contact the Compliance Team

Call : 01708 676110

Email : compliance@connectmortgages.

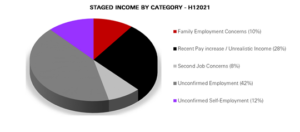

So, what do we mean by staged income, or even inflated income, and are these both types of fraud?

So, what do we mean by staged income, or even inflated income, and are these both types of fraud?

Staged income is the process of falsely presenting a job that doesn’t exist. This could be by creating fake payslips to make it look like someone has a job that doesn’t exist or amending bank statements to show money crediting an account that never did.

We also see companies that are complicit in this type of fraud by providing payslips for individuals that don’t actually work for them. This is common with family businesses.

These jobs will be recent and will usually have started between one to six months before they approach a broker. So, it is best practice to conduct additional due diligence on the following:

- Recent employment

- Second jobs

- Family businesses

So, how do we combat this?

There are many checks we can do to help identify staged income, such as:

- Ensure the fact-find has a full 12 months employment history.

- Ask for additional payslips and bank statements.

- Request HMRC Taxable income statement.

- Request employment contracts.

Other checks will include reviewing the location of the company and seeing if this makes sense for where your customer lives, to actually work there?

We have seen cases where people have a job, but it is 70 miles from where they live. This may make sense for someone on a high income as they will be more willing to travel for their job; however, this wouldn’t make sense for a shop worker on £25,000.

We have also seen cases where customers have two jobs. However, on closer inspection, it turned out they were both full-time and would require the customer to be in two places at the same time. Which isn’t possible.

Also, how do they get paid? Is this via a direct transfer into their bank account or do they get paid in cash? Most people are paid via transfers such as BACs payments or Faster payments, and in these situations regular cash payments will appear suspicious and should be investigated further.

But for certain jobs, such as shop owners or market traders, cash deposits into their bank accounts will make sense.

However, you can only know if the salary makes sense if you really know your customer.

Collecting documents and asking questions to fully verify the identity of your customers is called ‘Know Your Customer’ or KYC and is one of the best ways to reduce financial crime. For each case, you should be 100% comfortable that you know who your customer is and the information they have given you is correct.

So, what is inflated income?

Inflated income is where the employment is real, but the salary has been increased or ‘inflated’ to help obtain a mortgage that otherwise would not be affordable.

In these situations, all the documents will be genuine and will show the required income and will therefore look perfectly fine.

However, once the mortgage has completed, the salary will be reduced back to its original level. This is still fraud.

So how do we prevent this?

Whilst all of the documents we could request will show the required income, brokers can still conduct checks that will help reduce the potential of this type of fraud, this is where KYC or Know Your Customer is essential:

- Does their income level match that expected of that type of role or the size of the company?

- What is the turnover of the business? Could they sustain that level of salary?

- Is the income being spent each month or is it being left in the account?

Quite often with this type of fraud, the individual will have to pay back that money; therefore, it may remain untouched in their account. But think, how often do you see a salary go into a bank account and not get spent?

Lenders conduct further reviews after cases are completed, and if they see evidence that the salary was not genuine and has been reduced to a lower amount, they will flag this as a risk case against the broker and we have seen many examples of this.

As always, if you would like assistance or a second opinion on a case you are unsure of, please contact the Compliance team who will be happy to help.

Regards

Alan Baldwin

Director of Compliance

Ror any questions or queries, contact the Compliance Team

Call : 01708 676110

Email : compliance@connectmortgages.

We appreciate, as an adviser, you are aware that an essential part of your ongoing requirements for your annual fit and proper test, is to remain on track with completing your annual CPD.

As we reach the end of Q1, we’ve started to review individual YTD CPD totals. This is to check your status to ensure you are on track to avoid panic at the end of the year to catch up.

As a reminder, as of the end of Q1:

- If you have regulated mortgage permissions you should be on 375 Mortgage CPD points.

- If you hold only unregulated permissions, 150 CPD points.

- For insurance you should be on 225 CPD points.

Make sure you record everything!

We are aware that often you will have attended meetings, etc and not recorded it. So as a reminder, this can all be recorded on the LMS system HERE with just a simple press of a few buttons and uploading some notes.

If you need additional CPD content, we are constantly adding new material to LMS and very soon will be adding courses worth 16 hours of Insurance CPD which will cover the annual requirement!

Lender Digital Learning

For Mortgage CPD, log in to LMS and filter your courses to “Lender Digital learning” as below:

You will see CPD dashboards for the following Lenders & Insurance providers:

- Paragon Bank

- Accord/YBS

- LV – GI

- Source Insurance

- Livemore

- Virgin Money

- OSB Group (Precise & Kent)

- The Mortgage Lender (TML)

- Foundation HL

- Paymentshield

- Hodge

- Aldermore

More to go live soon ….

Additional External Sources

In addition to this, other external sources of CPD include:

- For insurance CPD – Protection Guru – https://protectionguru.co.uk/

- For Mortgage CPD – Financial reporter – https://www.financialreporter.co.uk/academy

Both of these sites have a huge amount of informative CPD articles that can be added using the process provided.

And finally, should you think you are struggling to find suitable material to complete your CPD, please contact the member support team at memberseupport@connectmortgages.co.uk who will be able to advise and direct you to the sources and material available.

Member Support Team: membersupport@connectmortgages.co.uk

Compliance Team: compliance@connectmortgages.co.uk

Do you have a Protection conversation with every customer?

Since we started using Elevation for customer feedback, we have been given a lot more information and insight into the customer journey.

Some of the key highlights on the Elevate reports are the questions around protection.

This has highlighted a number of clients that would have appreciated a protection conversation but didn’t receive one.

Following Consumer Duty, we enhanced our process on protection and introduced the mandatory requirement to complete the Insurance Your Needs tab on OMS. So long as this is completed as part of the fact-finding process, every customer will have a protection conversation.

But why is this important?

Should someone stop receiving a salary, even for a short period of time, they can quickly go into arrears with their mortgage lender and typically, lenders will start repossession proceedings after just three months of not receiving payments.

This is why protection is so important, but a conversation must take place for a policy to be sold.

Simply asking a customer about their savings and how long they could maintain their commitments should they lose their job is a great start to the conversation.

Whilst we have the questions on the Insurance Your Needs tab, this isn’t a script, and each adviser will have their approach to determining the need for protection.

Other questions to consider are:

- If they died, would their partner be able to maintain the mortgage repayments or would they like the mortgage to be repaid in full?

- How long will their employer provide full sick pay if they are unable to work?

- If they were to be put on statutory sick pay, would they be able to maintain their commitments including their mortgage?

These are all questions your customers may not have considered but should form part of your fact-finding process. The answers given will then determine if there is a need for protection.

For further information, we have a Protection Process guide in the Operations Manual.

This will help you with the protection process questions; however, if you have further questions, you can always speak to anyone in the Compliance team, who will be happy to help.

Observations

One of the changes we are making to assist advisers is introducing protection role plays.

This will either be as a stand-alone role play or included with the existing mortgage observations.

These role plays will then give us the ability to provide coaching and support that will, in turn, help you with having these conversations with your customers.

Training

Please remember that we run Protection training courses on a monthly basis that are free to attend for any existing adviser. So, if you feel you would benefit from re-attending this, please do not hesitate to contact the Member Support team.

Kind regards

Alan Baldwin

Director of Compliance

For any questions or queries, contact the Compliance Team

Call : 01708 676110

The Case Management team helps hundreds of cases progress, and they know all the tricks that can help your case complete quickly and with fewer declines.

So, what are these tips?

How to avoid delays

The biggest cause of delays that we see is OMS not being completed in full. This causes the team to contact brokers and ask for this information as it is required before the DIPS & Applications can be submitted. Information such as:

- Solicitors’ details

- Valuation/ Access Details

- Original Purchase Price and Date of Purchase

- Incomplete or missing client Identification, such as passport numbers

All fields in OMS are essential and mandatory; any missing sections have the potential to delay a case. So, if you want to avoid delays, spending a few extra minutes completing OMS will help your case greatly and get it to complete that little bit quicker.

We also see a lot of cases being delayed due to the adviser not having set up the required agency with that lender. When this happens, this can delay a case up to a week as it can take lenders this long to register the broker on their systems.

Therefore, when you are sourcing a product, ensure that you have agency, not just with the lender of choice, but the next two or three in the list as you may have to change the lender during the process.

How to avoid cases getting declined

The biggest cause of cases being declined that we see is the client not meeting the lender’s criteria, and these are things that can easily be checked before selecting that lender.

Credit Issues: lenders all have different appetites for credit, and this is always available on the lender’s website. So, ensure you review the client’s credit file for missed payments and make sure the lender accepts that level of defaults before you submit the DIP; never assume this will be checked during the DIP process.

Property Types: again, each lender has a different appetite for property construction. All lenders will be happy with standard brick construction, but what about other construction or build types such as:

- Timber frame

- Steel frame

- Poured concrete

- Flat roof

- Flats over five floors high

- Flats over shops

If you see something that is a little different from the normal, ensure you review the lenders’ criteria or if in doubt, speak to their BDM. For a little more information on the types of properties that lenders may not like, please click on this LINK.

With Mortgage Fraud a constant threat, we wanted to share some of the trends our Compliance team has seen recently.

Employment Fraud

A common type of employment fraud we have seen in the industry is inflated salaries whilst working for a family business, this is something that lenders look very closely at. This is due to the fact that income amounts can easily be inflated.

And what happens to these inflated incomes once the mortgage completes? As expected, this quickly reduces.

So, what can you do to combat this type of fraud?

KYC – Know Your Customer

KYC is the best way to help combat this type of fraud. KYC is the process of understanding the background of your client and their financial circumstances. Just doing some simple checks can help identify if what they have told you is genuine or not.

Conducting a Companies House searches will help you identify if the client has any connections with the company that they work for. Using this site, you can review all the people involved in the business and if their surnames match, then it is possible that the client is connected to the owners in some way. Also, using Companies House, you can review their financial accounts and review their turnover and size off the company. This is a good way to check if what the client has told you about their employer matches the truth.

Ensure you have collected at least 12 months’ employment history. In many cases of employment fraud, the client will only have been in their new job for a few months. Therefore, find out what they did before their new job or new role. Find out information such as:

- Has their income only recently increased?

- Are they being paid in line with the role and the size or turnover of the company?

- What is the distance between the job and where they live?

- Is their new job in line with what they were doing before?

- Are they connected to the owners in any way?

In each instance, you should ask yourself, does this make sense? Do I need anything further to support this case? If you are in any doubt, you can speak to Compliance before you submit, and they will be happy to help.

Unexplained Lender Declines

Sometimes, you may have completed all your checks, and you see no issues, but the lender still declines the case. When this is due to criteria, they will tell you just that, but sometimes they will decline without further information. This is usually a sign that they are aware of something that you aren’t. This can be intelligence from systems or other lenders that we do not have access to. But when a lender does decline your case, don’t just resubmit with another lender without doing additional due diligence.

Lenders have greater communication with each other than ever before and will tell each other about cases they decline due to fraudulent reasons. This means if you try and resubmit your case with another lender, it is likely to get declined again and your name could then get connected to the client in relation to the lenders concerns.

So, what can you do to combat this? Firstly, you should be asking your client during the fact-finding process if they have tried with any other brokers or had any applications declined? If the answer is yes, then you need to find out as much information about their previous cases as possible. If the declines are not property or criteria related, then they may need to find out what information is being held about them.

If a fraud flag is registered with a lender, it is likely to be held on one of the main fraud databases such as National Hunters, National SIRA or CIFAS. If your client wants to see what information lenders may hold on them, they can apply using the following links:

- https://nhunter.co.uk/

- https://www.cifas.org.uk/

- https://www.synectics-solutions.com/what-we-do/national-sira

If the flag is registered in error, then the client can contact them to try and remove it. Then once you are happy that all extra due diligence has been completed, you can resubmit the case.

If you have a case and you have any questions, or are unsure of what checks you should be doing, as always you can contact the Compliance team who will be happy to help you.

Regards

Alan Baldwin

Director Of Compliance

For any questions or queries, contact the Compliance Team

Call : 01708 676110

Nothing makes Compliance happier than telling someone that they have passed their file check. However, this isn’t always the case, but there are things advisers can do before they submit their case for checking that will significantly increase the chances of getting GREEN.

Some of the most common reasons that prevented cases from being graded green in 2023 were:

Proof if ID: Did you know an unsigned passport is invalid? and therefore not able to be used as Proof of Identification? This is a fairly new requirement on passports, so may not be something everyone knows. Further information on this can be found here LINK.

Bank Statements: You should be able to evidence the last three months’ worth of salary credits in the bank statements you obtain from the client. If only two appear due to the dates of the statements, then you need to request an additional one to ensure yourself and Compliance can compare the three salary credits to the payslips. Further information of the minimum documents that are required on cases can be found in the Operations Manual HERE.

Amended Documents: What checks can you as an adviser do to help identify potential fraud? Have you reviewed the opening and closing balance on the bank statements? We saw several cases in 2023 where these did not match, and this is an obvious sign that something in the statement has been amended. Fuzzy logo? Another clear sign that something is off with a bank statement is that the bank’s logo appears to be blurry. Ensure you are reviewing any document you receive from a client and if anything doesn’t seem right, call the Compliance team who will be happy to review for you.

Another great way to keep ahead of fraud trends is to attend one of the many lender webinars. HSBC runs monthly webinars that every Connect Network member must attend to maintain their agency with them. Not only are these mandatory, but they are also helpful in providing great information that will help you identify possible fraud.

If it isn’t written down, it didn’t happen: Your case should tell the story of your interaction with the client. There have been many occasions where we will query or request something and it turned out that it already happened, but it just wasn’t noted on the case. If you have done extra work to verify a client’s employment, remember to upload the document or note it on the file. This causes many cases to get declined by lenders and some of these would have been accepted if the story was told.

Protection Conversation: Whilst having a protection conversation has always been part of the sales process, Consumer Duty has put even more emphasis on this requirement. It is now mandatory that every regulated case has the Insurance Your Needs section completed in full. This also needs to be completed if you aren’t doing the advice yourself and are instead referring the lead to Stonebridge.

Following the implementation of the Vouchedfor client feedback process, we have been able to get a far greater insight into potential customer detriment, and we have seen that we have many clients who would have liked to have a protection conversation but didn’t. This is why it is so important to cover off the Insurance Your Needs tab during the fact-finding process, as this will identify clients who would like to discuss protection further.

Lastly, the best thing you can do to ensure you have covered everything you should have, is by completing the File Check tab on OMS, if you have covered off every area on this tab, you are far more likely to receive a Green file check, first time.

Regards

Alan Baldwin

Director of Compliance

For any questions or queries, contact the Compliance Team

Call : 01708 676110

As part of our ongoing commitment to regulatory compliance, we would like to bring your attention to the upcoming Annual Financial Data Request mandated by the Financial Conduct Authority (FCA). For those who have been affiliated with Connect for over a year, you may recall receiving a similar form last year.

The FCA requires the submission of this information on an annual basis, and it is now time to initiate the process once again. This data request will be directed to the controller of each firm, who is expected to complete it on behalf of the entire organisation.

This data request involves updating your principal firm (Connect) of all the following:

1) Total Regulated Revenue (outside of Connect)

This is all revenue generated from regulated activity, such as:

- Regulated mortgages

- Personal Protection and GI

- Equity Release

- Commercial mortgages to individuals

- Consumer BTL

- Regulated second charges & Bridge loans

2) Revenue generated from Financial Non-regulated activities (outside of Connect)

Any activity of a financial nature that does not involve the person carrying on regulated activity. This would include, but not limited to, revenue from activities such as:

- investment services

- insurance

- pensions

- banking

- lending (including consumer credit, mortgages, factoring, financing of commercial transactions)

- financial leasing

- money transmission

- payments

- guarantees and commitments

- foreign exchange

- the issuance of securities and other service of a corporate finance nature

- custodial, depositary and trust services

- financial information and data services

3) Revenue Generated from Non-Financial Non-Regulated activities (i.e. all other business)

This includes, but is not limited to, revenue generated from running any of the following activities, this does not include referral fees received:

- Running an Estate Agency Business

- Property Sales

- Solicitors

- Accountancy

For each category, a comprehensive explanation of the type of business and corresponding revenue is required.

When do you need to complete this?

We will shortly be sending this form out via email to each controller to complete and return.

This information must be returned to Connect within two weeks of receiving the request, which will be issued shortly, so you may want to start preparing the information.

If you have any questions in relation to this, please contact me directly.

Kind Regards

Alan Baldwin

Director of Compliance

For any questions or queries regarding this email, please contact Member Support Team

The next batch of emails will shortly be going to your completed mortgage customers from Elevation. As a reminder, these emails will be as if you had sent them, but will be sent automatically for you from the Elevation system.

You should by now have received your login details directly from Elevation, and you will receive an email whenever a customer completes feedback so you can review it.

Reminder, Consumer Duty Requirements

As a reminder, Consumer Duty requirements mean all Networks need to ensure they are able to measure that the advisers they supervise are meeting the new requirements of the Duty. As previously communicated, Consumer Duty means we need to provide actual evidence that shows we are putting customers at the heart of the business. Many advisers do have review facilities such as Trust Pilot or Google reviews. However, the FCA has indicated that a good review does not in itself satisfy their requirements in evidencing that good consumer outcomes have been delivered.

Why Elevation?

Some networks have chosen to telephone customers and ask questions to obtain this evidence. We have chosen Elevation as we believe it is also a great tool for our members. Elevation by VouchedFor is different from a normal review service in that it asks a range of questions to fully understand the customer’s experience. The information from this gives both the network and the adviser the ability to understand the journey from the client’s perspective, as well as evidence the good outcomes or learn where improvements can be made.The insights the adviser gains can increase conversions, business levels, and personal recommendations.

Launch Webinars

In September, we invited all members to attend one of 2 webinars with the Elevation team so that advisers would understand what was happening and why. If you did not manage to attend the webinar, you can view a recording of it here:

Feedback Request Email

The feedback request email sent to your customer by the Elevation system is addressed from you because your customer knows you. This means a higher response rate. To maximise the benefits, it’s a good idea to let your customer know that they will receive it. We are currently scheduling requests for completed mortgages, but in due course, we will schedule requests at earlier stages in the process. This is incredibly powerful, as it will provide you with insights on why some customers do not proceed with an application.

All advisers have access to a free account with Elevation to see their feedback. There is also an option to have a personal VouchedFor profile to display the customer rating part of the Elevation feedback at a discount to the normal price. This is similar to services like Trust Pilot and Google Reviews but can also help you with lead generation through their free ‘find an adviser‘ service.

If you would like any further information, please reach out to the Member Support Team in the first instance.

Kind Regards

Alan Baldwin

Director of Compliance

For any questions or queries regarding this email, please contact Member Support Team

Referral Partners

We’re delighted to remind you about our carefully vetted network of partners, to whom you can confidently refer business that falls outside your scope of permissions or expertise. These partners have met our exacting due diligence standards to ensure your clients will be treated fairly, and their fees are fully aligned with the FCA’s Consumer Duty guidelines.

To maintain the highest quality of service and compliance, we kindly ask that you continue directing all client referrals exclusively to these approved partners. If you have any questions or need additional guidance, your Business Relationship Manager and I are always available to assist. Thank you for your ongoing commitment to excellence and compliance!

Please do not hesitate to contact your BDM or the Compliance Team for further information or guidance.

Kind Regards

Alan Baldwin

Director of Compliance

or any questions or queries, contact the Compliance Team

Call : 01708 676110

Email : compliance@connectmortgages.co.uk

To assist you in meeting the requirements of The Consumer Duty, we have created a new tab on a client record in OMS called ‘Consumer Duty’.

This tab should be treated as an ‘aide memoir’ of the principles of The Consumer Duty and the areas that advisers need to consider in all their dealings with their clients.

This includes:

- Vulnerable customers

- Foreseeable harm

- Customer Understanding

- Fairvalue

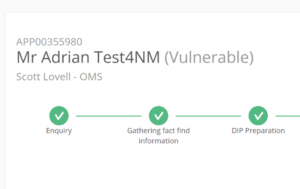

Should the answers indicate the client is potentially vulnerable, you will be directed to turn on a vulnerability flag by completing the section at the bottom of the applicant details tab.

When you tick yes to one of these questions, the word ‘Vulnerable’ will appear against the client’s name as seen below:

The vulnerable flag against your client’s name will only be seen by yourself and the internal team and will not be seen by the client if you use the customer portal.

Forseeable Harm

Further information on the FCA requirements for each of these areas can be found in BOX. We have also written a recent blog specifically about foreseeable harm.

For mortgage advisers, this means taking steps to ensure that they know their clients well, understand their short and long-term needs, recommend the right products and services to their clients and provide them with clear and accurate information.

Read the blog ‘How to Avoid Causing Foreseeable Harm as a Mortgage Adviser’

to see specific examples of what could be deemed to be foreseeable harm.

Please do not hesitate to contact the Compliance Team for further information or guidance.

Kind Regards

Alan Baldwin

Director of Compliance

For any questions or queries, contact the Compliance Team

Call : 01708 676110

Email : compliance@connectmortgages.co.uk

You may have heard a lot about lender and provider fair value statements, some lenders may also have sent those to you, and you are wondering what you need to do with them.

You will be pleased to hear that it is the responsibility of the Network to review these for the lenders we have on our panel.

As part of Consumer Duty, we have collated the Fair Value Statements and completed an assessment to check that the product appears fair and that the target market for the product is consistent with the customers our advisers are recommending the product to. We have also looked to consider if there are any characteristics of the product that make the product suitable or unsuitable for vulnerable customers.

This is an ongoing piece of work, as lenders launch new offerings. We will be conducting lender reviews on a minimum of a yearly basis, and in some cases as frequently as quarterly for some of our most used lenders.

The purpose of these fair value statements is for them to be reviewed at the Network level and not at the individual customer level.

So while copies of these will be available from the lenders, their websites, BOX and the sourcing systems, you are not required to add these to the customer file on OMS and you must not give them to customers.

Therefore, there are no changes at this time to your current research process, meaning the selection of mortgage lenders should still follow the ‘Cheapest Rule’ requirements.

For protection, Connect belong to the Genus Protection Club, which offers a ‘loaded panel’. This means that the customer is charged a higher premium than may be available by the customer directly so that the commission for the adviser can be higher to reflect the work involved.

We have completed a re-assessment of this panel offering as part of Consumer Duty. At this moment in time, we are satisfied that the additional advice and services the customer benefits from when using an adviser still represent fair value under the Genus panel. However, for any adviser still operating under the old ‘non-advised’ model, we will have already been in contact to help you to switch to the fully advised model.

Fees Policy

Following the previous communication about fees, there have been a couple of questions, so I will just touch on those themes.

Some of you are concerned about the cap that will be applied to the fees you can charge. It is important to note that the fair value of broker fees is being driven by the FCA rather than Connect.

The feedback we have received is that the caps being applied by the larger Networks are considerably lower than the Connect offering, and in many cases, the Networks are not allowing percentage fees.

We have also adopted a tiered approach which means a higher cap for the more complex products, and for the majority of the unregulated mortgage products, there is no cap.

As part of Consumer Duty, this is being monitored by lenders. For example, lenders like Coventry send us regular reports detailing specific cases where the fee is more than 1% of the mortgage, regardless of whether it is Residential or Buy-to-Let.

To support all advisers, while we have issued this guidance, we are of course happy to consider individual requests either on a case-by-case basis or where the Network Member can provide their own acceptable fair value assessment of a different fee and service model.

You can view the guidance again in more detail in BOX

NETWORK FEE GUIDANCE: View Here

SETTING YOUR OWN POLICY: View Here

If you need any further assistance, please do not hesitate to contact the Compliance team: compliance@connectmortgages.co.uk

Kind Regards

Alan Baldwin

Director of Compliance

Call : 01708 676110

Email : compliance@connectmortgages.co.uk

We are just a few weeks from the final implementation date for Consumer Duty.

Over the next few weeks, I will be sending you regular Consumer Duty emails, like this one, covering some of the updates the Network has made in readiness for meeting the Consumer Duty.

The Duty introduces new rules and guidance to ensure that:

- Products and services: are designed to meet the needs, characteristics and objectives of a specified target market

- Price and value: Products and services provide fair value with a reasonable relationship between the price consumers pay and the benefit they receive

- Consumer understanding: Firms communicate in a way that supports consumer understanding and equips consumers to make effective, timely and properly informed decisions

- Consumer support: Firms provide support that meets consumers’ needs throughout the life of the product or service

In this email, I will cover fees that you charge and how that impacts the Consumer Duty Price and Value requirement.

Fees And Fair Value

It is important to note The Duty applies to regulated mortgages. This includes regulated Buy to Let, such as Consumer and Family Buy to Let. However, as a regulated firm, we have also considered The Duty when creating our approach to the non-regulated products we offer consumers.

The Duty does not have a retrospective effect and does not apply to past actions by firms. However, the Duty applies, on a forward-looking basis, to firms’ ongoing work for existing customers.

The FCA confirms:

A mortgage intermediary must ensure that its own fees and charges offer fair value and that payment of these does not result in the product or service ceasing to be fair value overall. Firms should not exploit customers by, for example, charging unjustifiably or unreasonably high fees or charges to more vulnerable groups of customers such as those with a poor credit history or older customers.

Firms need to ensure they are providing consumers with the information they need to make informed choices and understand the costs involved. Firms should consider their fees and charges in the context of the Duty and consider what steps they may need to take. In particular, firms should review their services and pricing to satisfy themselves that they are offering their customers fair value.

The Connect Network Fee Policy

The work required under fair value sits with the Network creating a fair value framework, ensuring the services it provides and the products it distributes are fair value and that its distribution arrangements do not affect the overall fair value (for example, as a result of a broker fee).

We have collated and reviewed the fair value statements for the lenders and providers on the Network panel. We will be monitoring the lenders and providers on our panel to ensure that they meet the standards we expect to deliver good outcomes for our customers. We have also reviewed some of the fees that our Member Firms charge in light of the new rules and completed our own assessment of the fair value of fees using services typically offered by our Network Members.

Many of you offer complex and specialist advice and hold a level of lender and criteria knowledge that is higher than a typical mainstream-only mortgage adviser, which we wanted to consider when setting the Network fee policy. We are mindful of the FCA statement that firms should not exploit customers in more vulnerable groups, such as those with a poor credit history. However, we do feel that a higher level of expertise and a more detailed research and application process for complex cases does need to be recognised. (We will be communicating in due course additional work we are doing to identify and support vulnerable customers.)

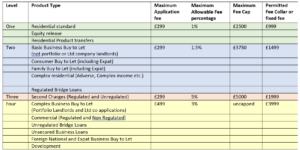

The Network has adopted a tiered approach in relation to fees. This policy specifies the Network’s maximum fee tolerances for different product types as per the table below:

We do not expect all advisers to charge the maximum, these are just the maximums allowed without the need for the Network Member to refer to compliance for pre-approval.

More details and a fuller explanation can be found in the full document in BOX here:

When we complete our Annual Fit and Proper assessment with each firm, moving forward, we will be asking you to outline your firm’s own fee-charging policy and how you believe your fees and services offer fair value to your customers.

To assist you in thinking about this, we have created some guidance and tools, which can also be found in BOX here:

If you need any further assistance, please do not hesitate to contact the Compliance team.

Kind Regards

Alan Baldwin

Director of Compliance

For any questions or queries, contact the Compliance Team

Call : 01708 676110

Email : compliance@connectmortgages.co.uk

To improve our compliance process and to allow cases to progress quicker, we have decided that for advisers working towards CAS status, we no longer require cases to be submitted to Compliance for Pre-DIP checks.

Compliance will instead check cases at the pre-application stage for those who have not yet received Competent Adviser Status (CAS). After achieving CAS, the team will continue to complete quarterly case checks for all advisers on mortgages that have been completed.

This,however, does not change our Network requirement to have cases correctly packaged before you submit a Decision in Principle (DIP). Compliance will conduct spot checks on cases at the DIP stage to ensure minimum document requirements are still being adhered to. This is important to ensure that your DIP to APP success ratio is within expected lender standards.

How will the process work?

To ensure we are still maintaining an appropriate level of control, there will still be a requirement for some advisers to have DIPs processed by the Case Management Department as below:

- ACADEMY For Academy advisers, all cases must be submitted to the case management team for processing until CAS status has been achieved. A minimum of 6 months and a minimum number of cases apply before Academy advisers can complete DYA training to submit their own cases.

- EXPERIENCED For experienced advisers (those with 12 months or more industry experience and previous CAS status), the adviser must submit their first case to Case Management to process. To be able to submit your own DIPs going forward, thiscase must pass the Case Management case review, and the adviser must completethe DYA training. The team will then confirm that you can submit your own DIPs.

You can notify compliance to complete the pre-application review at any time after the DIP is completed.

If there are any DIPs currently waiting for a Compliance review, we will contact all advisers to confirm that the case can be submitted to the lender. These cases must, however, still be sent to compliance for a pre-application check before the full application is submitted to the lender.

Timescales

These changes will take place with immediate effect. If you have pipeline cases, you will receive a confirmation email from Compliance.

We are listening

We are also introducing an updated grading system, which will mean some cases we currently class as Amber may still be able to achieve a green pass, with minor errors. There will be 6 levels of grading as follows:

6-Green Advice is suitable, and the file is complete with no missing documents or information.

5-Green Advice is suitable, but there are minor fact-find omissions or document omissions (not minimum standard documents) but the omissions are not affecting the advice.

4-Green / Amber Advice is suitable, but some documents evidencing advice are missing, or the suitability letter is presented with minor omissions. Rated as amber-4, but upgraded to green-5 if corrected within 48 hours.

3-Amber Advice is suitable, but minimum one or more company standard minimum documents are missing, or the suitability letter is presented to the customer with material omissions on the recommendation, requiring re-issue.

2-Red Unsuitable advice, eg. mortgage unaffordable, product does not suit customer needs, justification for the advice not clear. (If acceptable justification and correction are provided within 48 hours, upgraded to Amber-3)

1-Red Suspected fraudulent case, e.g.Back door residential, staged income, fraudulent documentation etc.

Your total points over a quarter will be averaged and used to identify overall training and support needs.

I hope these initiatives show that we are listening to feedback to help all our members to get compliance right for the customer without unnecessary burden.

If you have any questions about this new process, please contact me or the Compliance team directly: compliance@connectmortgages.co.uk

Kind Regards

Alan Baldwin

Director of Compliance

For any questions or queries, contact the Compliance Team

Call : 01708 676110

Email : compliance@connectmortgages.co.uk

Unfortunately, we have seen an alarming increase in mortgage fraud recently, particularly relating to income fraud.

A number of cases have been presented that advisers may have prevented with better due diligence.

Staged income is one area we have seen an increase. For example, a customer has got a recent wage rise which is quite a big jump in income and happens to be the amount they need for the affordability to work. Often there is a family connection, e.g., they work for a family business, making it ‘easy’ for applicants to receive a temporary wage increase which is not real.

Another area is around second jobs, e.g. a recent second job has been taken, with the income needed for affordability. Often the amount of working hours in total is not plausible, and/or they have been employed by a family member.

Lenders are sharing more and more risk data and also looking at applications post-completion. They will check, for example, with the client’s bank if the income has been and continues to be received at the level declared on the application.

Application flags

When there are any flags on an application, e.g. 2nd job, the employer is far away from the applicant’s home, a big pay rise, employed by the family, the applicant appears to earn more than the employer, then the lender will increase the questions and documentation requests. This can indicate there is a concern. Of course, just because there is a flag, does not mean this is not a genuine application. You can avoid any misunderstanding by making sure when the application is submitted that more detail explaining the applicant’s circumstances that may mitigate the risk, is provided upfront.

It’s incredibly important to respond to any requests from the lender for documents, even if the case is not proceeding. Make sure you tell the lender exactly the reason why the case is not proceeding. Failure to do this can mean the lender attaches a suspicion against the case and the adviser, where there is not one.

Sending a client’s application to multiple lenders to see what ‘sticks’ will also earn you a red flag from a lender, which is why this is not tolerated by the Network. As will continuously misunderstanding the lender’s criteria and submitting cases outside of their policy.

Lender Expectations and Panel Removals

The lender expects an adviser to know their customer and complete detailed due diligence on all information and documentation with due care and knowledge. Fraudsters can be quite sophisticated, which is why we created the ‘risk checks’ on OMS to help guide you on what to look out for. Every time a lender blocks a potentially fraudulent application that you have not spotted, this increases the lender’s risk. If this continues, or if post-completion fraudulent cases are uncovered, the broker will be removed from the lender’s panel.

If you are removed from one lender’s panel, this information is shared with the FCA and other lenders, and you may be subject to further panel removals from other lenders simply because of the first lender removal.

This means the Network would have no alternative but to terminate your contract, and you will no longer be able to submit any mortgage business.

Further information and training

Liz recently wrote a blog which can be seen here

More information and training can be found in LMS, and both the compliance and member support teams can assist with individual case queries.

HSBC are also running a virtual fraud training session on Wednesday 31st May at 9.30am, you can register here

Kind Regards

Alan Baldwin

Director of Compliance

![]() In order to help combat financial crime and to reduce the number of fraudulent applications HSBC has seen in the industry lately, we have agreed with them to make their fraud training webinars, which are being hosted just for Connect IFA advisers, mandatory for all staff with agencies with HSBC.

In order to help combat financial crime and to reduce the number of fraudulent applications HSBC has seen in the industry lately, we have agreed with them to make their fraud training webinars, which are being hosted just for Connect IFA advisers, mandatory for all staff with agencies with HSBC.

Whilst being mandatory for advisers, this is also open to any staff who would like to attend because they expect to request a HSBC agency soon or they are keen to understand more about fraud to protect their business.

You can register below for webinar being hosted 31st May, by following the appropriate link below.

If you have an HSBC agency and wish to continue to use it, you must attend.

If the date is a problem, please advise and we will arrange an alternative for you to attend.

Please note these events will be accessed via Zoom.

- Wednesday 31st May- 9:30an – Zoom Link

If you have any questions, please contact Compliance.

Kind Regards

Alan Baldwin

Director of Compliance

For any questions or queries, contact the Compliance Team

Call : 01708 676110

Email : compliance@connectmortgages.

As the new year begins, this email is to inform you of some changes being made to the CPD requirements for the new year and how we are making it easier for you to record your CPD. We have also made some changes to the CFI Members Folder and Operations Manual to make it easier for you to find the information you need for your day-to-day mortgage business.

CPD

As mentioned previously, we are removing the blanket 40 hours of CPD and the requirements will now more closely align with the permissions you hold, full details of which can be found HERE.

Over the coming months, we will be continuing to build the CPD library on LMS to have additional lender-specific knowledge at your fingertips, together with more general industry and product oversight.

Any activities you complete within LMS automatically add CPD points to your record.

For CPD activities you undertake outside of LMS, e.g. external courses or events, or BDM visits to your office, we have made it easier for you to record these.

In LMS you will find THIS COURSE which will allow you to select the amount of time the CPD activity was for and simply upload evidence of the activity to claim your time. You will see going forwards that when you have selected an amount of time and completed it that it will show as “completed”, but you can revisit it and complete it several times over the year (for example, you can complete multiple 60 minutes mortgage CPD sections over the year)

To avoid the rush at the end of the year for CPD points, the member support team will aim to remind you regularly where you are against your CPD targets, and provide guidance on how you can keep on track. Please remember, however, your CPD completion remains your responsibility and is a contractual and regulatory responsibility.

BOX CFI MEMBER FOLDER AND OPERATIONS MANUAL

To make it easier for you to find information needed to answer any questions you have about running your mortgage business, we have taken the PDF operations manual and moved it into individual pages in folders within the CFI member folder.

At the same time, some information has been added, removed and updated to make it the most comprehensive source of information from sales processes to commissions to compliance and more.

You can use the BOX search function to search for any files that contain the information you are looking for:

I’m sure you will all agree both of these are positive steps in supporting you with your business. If you have any questions, please contact member support for assistance.

If you have any questions, please contact member support for assistance. membersupport@connectbrokers.co.uk

Regards

Liz Syms, CEO

Consumer Duty

Consumer Duty

There is a lot of press in the industry about Consumer Duty and what this means to advisers. I can confirm that as the Network Principal, Connect is required to interpret the new standards and implement any requirements across the network. Network members are not required to consider what action is to be taken, as any changes needed will be decided by the network. So you do not need to worry and we will be communicating to our members any changes within plenty of time to meet the deadlines required.

I can confirm that the Connect Network Senior Management Team have approved the first draft of the network Consumer Duty implementation plan. We believe we are in a good place and already meeting many of the requirements, but some areas are under review for enhancement for the benefit of consumers. These include our vulnerable customer processes, protection sales processes and our policies and procedures documentation.

Over the coming months, we will communicate any changes to our processes that you need to be aware of and make available training and support so that we are fully prepared for when the Consumer Duty Rules come into force in July 2023.

In the meantime, the date for the implementation of PS22/11 ‘Improvements to the Appointed Representative Regime’ comes into force on the 8th of December and forms a part of the overall Consumer Duty requirements.

Improvements to the Appointed Representative Regime Paper

Our review of the paper has been completed and in the coming weeks, we will be implementing some changes to ensure the network meets all the new requirements ready for the start date of 8th December.

These changes include the following:

Contract

In the next couple of weeks, we will be issuing a new contract that will need to be electronically signed by the controller of each firm. This is to include new wording required by the FCA, which requires appointed representatives to cooperate fully with the FCA including granting access to premises. We are also required to add a paragraph that gives access to the network to as much information, without limitation, as necessary for us to comply with its own obligations to the regulator, including reporting and notification obligations.

At the same time, we will take the opportunity to complete some minor adjustments and amendments to the contract to improve clarity.

The updated contract will come from BOX and we will also advise you by email when it is issued.

Operations Manual

The operations manual is in the final stages of a full update and will be launched in BOX to correspond with the issue of the new contract.

This will ensure that you have easily available the most up-to-date supporting information you need to meet your obligations under the contract and to the FCA.

CPD

From 2023, we will be making it easier for you to do your CPD or record your external CPD in LMS, with quarterly rather than yearly updates. This will remove the pain of annual record reconciliation and demonstrate the consistency of your learning to the regulator.

15 hours is the minimum regulatory CPD requirement for advisers with protection permissions so this will be retained. 40 hours is the suggested target for mortgages, but we will be breaking this down by product permissions. This means advisers holding permissions from say just one product line, will have more appropriate and focused CPD minimum requirements.

Monitoring

We will be updating our application process and annual fit and proper process to meet the new requirements. This will include asking for additional supporting information such as bank statements, company accounts and business plans. In February will be required to provide full financial income data for all our appointed representatives both for the business they undertake at Connect and also for any other business transacted through the same entity, but not through Connect.

We will be looking to gather the data to meet this specific requirement in early January and the data required will cover the full calendar year from January 2022 to December 2022. We will provide more information in relation to what this looks like when the final requirements are published by the FCA on the 8th of December.

We have always taken pride in the bespoke offering we have for Network members, which we wish to try and maintain as far as possible. However, due to the new rules and increased scrutiny from the FCA, we may not be able to offer as much flexibility in our approach as we may have done in the past.

Whether you are looking to complete your annual fit and proper or take on new members of staff, we will look to provide as much support as possible to help you understand the new requirements.

If you have any further questions, please contact compliance@connectmortgages.co.uk